[ad_1]

Most investors are risk averse, leading them to dislike securities exhibiting negative skewness (longer/fatter left tails, with the risk of a large loss), creating a risk premium for those securities. Assets with negative skewness are associated with higher expected returns. However, as skewness increases and becomes positive, the relation between volatility and returns becomes negative—investors may accept low returns and high volatility because they are attracted to high positive skewness. This is referred to as the “lottery effect”—a large chance of a negative outcome, with a small chance of an extreme positive outcome).

Attracted by the low nominal price of options (providing leverage) and their lottery-like potential outcomes, along with the perceived potential for generating quick profits, trading in options by retail investors has exploded. Most options trades by retail investors are buys, as they have positive skewness (the lottery-like distribution), while sells have negative skewness (the profit is limited to the size of the premium). The recent practice of charging zero commissions has also encouraged trading. Payment for order flow (PFOF), whereby the market makers to whom a brokerage firm routes its orders for execution pay for the orders they receive, pioneered by the mobile app Robinhood in 2015, creates an incentive for brokerages to encourage investors to trade more and to trade assets with larger spreads. That is why the opportunity to trade options is displayed prominently on gamified investing apps used by the new generation of investors—likely to their detriment. In 2021 the annual PFOF from options was $2.4 billion compared to $1.3 billion from equities.

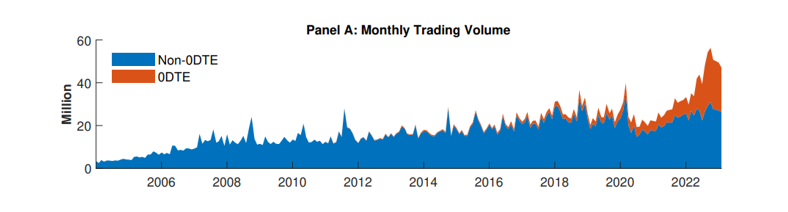

Because retail investors love the low nominal price of options, same (zero) day options are appealing because the shorter the time to expiration, the lower the nominal price. To that end, in 2005 the Chicago Board Options Exchange initiated a pilot program that introduced weekly options with expiration dates on each Friday. In 2016, Monday and Wednesday expirations were added. And in May 2022, it introduced options that expire on each weekday.

Recently, so-called “0DTE” options (short for zero days to expiration) represented more than 75% of the total volume retail investors transacted in S&P 500 Index options. Almost the entire growth in S&P 500 options trading over the last few years can be attributed to these ultra-short-term contracts.

Helping to create the speculative demand are numerous websites aimed at teaching retailers how to trade these options, and “0DTE” is frequently discussed on the popular wallstreetbets forum on Reddit.

Are retail investors benefiting from these innovations, or are the winners the exchanges and broker-dealers (the “casino operators”)? Heiner Beckmeyer, Nicole Branger and Leander Gayda, authors of the March 2023 study “Retail Traders Love 0DTE Options… But Should They?,” sought to answer that question. Their full data set of intraday trade data started in January 2005 and ended in February 2023. Their data set of 0DTE options spanned the period January 2021-February 2023. Here are their key findings:

The total share of retail trading of 0DTE options exceeded 6%, and around 75% of all retail trades in S&P 500 options were in 0DTE options. More than 40% of all traded contracts expired on the same day, and most positions in those ultra-short-term options were closed before maturity. Retail investors also favored small order sizes, with 72.2% of all orders trading a single option, 25.2% trading between two and five options and only 2.6% trading between six and 10 options.

Effective spreads were lower for retail trades: 6.1% for calls and 4.9% for puts compared to 13.1% and 10.1% for non-retail trades. Non-retail investors prefer to trade in small lots because of market impact costs. However, more than half of their volume was transacted through orders of 11 or more contracts. Despite spreads widening as the option approached expiration, retail investors continued to trade 0DTE options with less than an hour until expiration.

Retail investors bought more 0DTE options than they sold—leaving the options market maker with a net-short position. The aggregate net-short position of market makers in 0DTE options has grown considerably in recent months. Option market makers’ hedging activity has the potential to exacerbate intraday market swings.

Retail investors consistently lost money. Across the sample period of a little over two years, retail investors lost more than $70 million. Retail losses from 0DTE options have grown over time, especially since the introduction of options expirations on every weekday. While average daily retail losses were $184,000 for the entire sample, since May 16, 2022 (the introduction of a daily expiration calendar), daily retail losses grew to $358,000. About 60% of daily losses were the result of transaction costs, 60% were driven by investments in 0DTE put options, and retail buys showed particularly poor performance (buyers of options pay the variance risk premium and have negative expected returns even before expenses).

While long positions in options lost money on average, short positions were profitable even after fees (by providing insurance, sellers can capture at least a portion of the variance risk premium). While the average long position of retail investors lost 53% of its value across the full sample and 61% for the sample since May 2022, selling insurance earned a large premium for the average trade, with returns of 48% and 56%, respectively. Unfortunately, retail investors were more often long than short, resulting in net aggregate losses.

Ultimately, market makers profited from retail demand in 0DTE options through high levels of fees, larger than for the remaining retail orders, including short-term options with only a week to expiration.

Their findings led Beckmeyer, Branger and Gayda to conclude: “Retail traders exhibit a strong preference for high-risk, lottery-like assets and have found the perfect investment vehicle in 0DTE options.” Unfortunately, it seems they fail to account for the considerable spreads they incur when trading. “Their hunger for lottery-like assets leads to large aggregate losses.”

The authors’ findings are consistent with those of Svetlana Bryzgalova, Anna Pavlova and Taisiya Sikorskaya in their April 2022 study “Retail Trading in Options and the Rise of the Big Three Wholesalers.” They analyzed the options trading of retail investors and its profitability and found that from November 2019 through June 2021, after trading costs retail trades lost more than $4 billion! They concluded “retail investors’ motives for trading appear to be gambling and entertainment and that they incur substantial losses on their options investments”—much larger than their losses on equity trades.

Investor Takeaways

Elimination of commissions has fueled a retail participation boom in financial markets, a rise in day trading and the “gamification” of investing. The success of the zero-commission business model relies on payments for order flow from intermediaries that execute retail orders. That model incentivizes brokerages to induce more trading. Given that retail investors are basically uninformed and are drawn to lottery-like investing, wholesalers (like casinos) are extracting billions in spreads from the pockets of naive individuals. Because bid-ask spreads on options exchanges are considerably higher than those on stock exchanges, market makers that receive retail buy and sell orders are likely to benefit more from executing transactions in options, often crossing those trades. Adding to the losses caused by expensive trading is the failure of naive retail investors to optimally exercise options.

Larry Swedroe has authored or co-authored 18 books on investing. His latest is Your Essential Guide to Sustainable Investing. All opinions expressed are solely his opinions and do not reflect the opinions of Buckingham Strategic Wealth or its affiliates. This information is provided for general information purposes only and should not be construed as financial, tax or legal advice.

[ad_2]