[ad_1]

While the collapse of Silicon Valley Bank spurred fears about its effects on regional banks, broker/dealers and advisors affiliated with them are navigating the fallout, with more scrutiny and worry to come for regulators and clients alike.

While those reps work to keep clients (and their assets) at their bank, as well as independent advisors who custody asset at a bank, Carlo di Florio, a global advisory leader with ACA Group, urged reps to weigh their own risk management in the wake of SVB’s downfall.

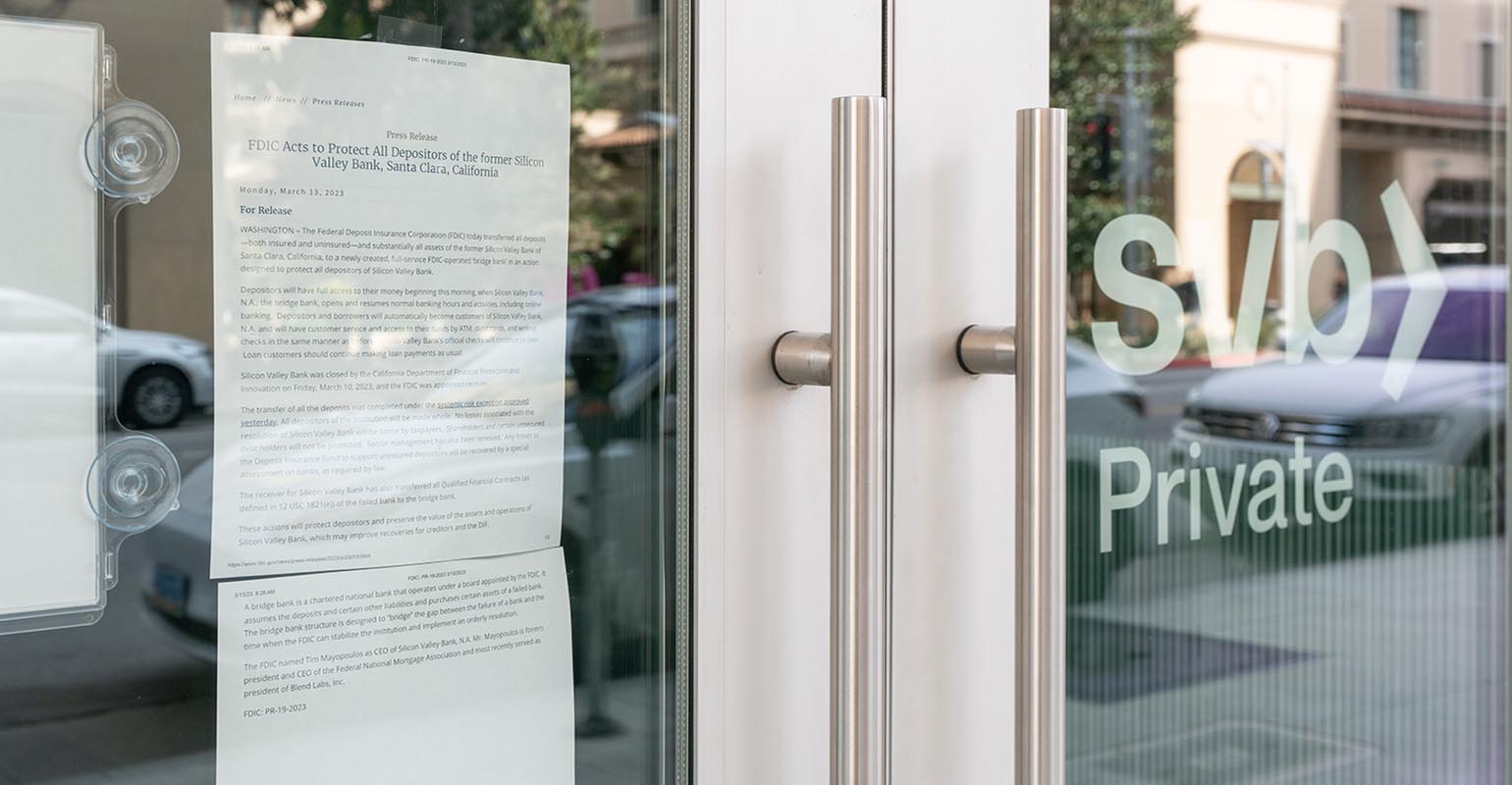

Regulators seized SVB earlier this month and it became the largest U.S. bank to collapse in more than 10 years, and the country’s largest since the Great Recession. While many of SVB’s deposits were well above the $250,000 limit imposed by the Federal Deposit Insurance Commission, regulators announced they’d fully insure all depositors, hoping to prevent additional turmoil.

Other banks faltered following the news at SVB, including First Republic (which got a reprieve via a $30 billion cash injection from financial institutions), as well as Signature Bank. This weekend, UBS announced it would buy the beleaguered Credit Suisse in an effort to stymie global concerns.

SVB’s downfall left many worried about regional banks’ vulnerability. The affiliated brokers and advisors at those banks are subject to securities regulators, and have to maintain separate capital and segregate client accounts. But di Florio believed regulators will be watching closely to ensure that banks under pressure don’t opt to illegally use brokerage and advisory assets as a “piggybank” to paper over financial stress, even if they intend to do so only temporarily.

“That’s the risk scenario, and the way that manifests if you’re a broker/dealer or investment advisor inside one of these banks, is it’s very likely you’re facing a whole lot of scrutiny from SEC and from FINRA right now,” he said. “They’re watching very closely to make sure that doesn’t happen.”

Banks and their affiliated reps are worried clients with investment accounts would respond to the past week’s headlines by moving their business elsewhere, deciding a potential bank shutdown wasn’t worth the risk.

Di Florio said he was concerned about the race away from regional banks and toward the Big Four wirehouses, perceived as being more secure, despite little immediate indications that SVB (and the tumult at Signature and First Republic) would cause regional banks to topple.

If smaller and regional banks suffer, the country’s economy could take the hit, he said.

“They fill a role the big banks don’t,” he said. “If everyone runs into the Big Four, what implications could that have on our economy, to lose these kinds of middle market regional banks?”

But di Florio hoped government efforts to make SVB depositors whole will staunch the bleeding and lessen pressure on bank-based reps, and clients, to flee to perceived safety.

“It’s to calm, comfort and avoid a bank run,” was the message he hoped those moves conveyed. “The institution of which you are a part will continue to be financially safe and sound and viable. You’ll continue to be able to do your investment advisory business and broker/dealer business as a part of that institution.”

Approximately 8.4% of the industry’s advisors were affiliated with a retail bank broker/dealer as of the end of 2021, according to Marina Shtyrkov, an associate director with Cerulli Associates. The group defined retail bank b/ds as retail bank branches, (excluding trust departments and private banks) or third-party marketing firms offering brokerage services to small banks. This contrasts with RIA channels, which accounted for about one quarter of the country’s total advisor headcount.

Gary Zimmerman, the founder of MaxMyInterest and former Citigroup managing director, said he didn’t see “massive systemic risk” in the banking sector, or a big custody risk on the securities side.

To Zimmerman, whose firm automates cash deposits across a number of banks in pursuit of the best interest rates for clients, the risk comes from cash sweep systems, in which a brokerage firm would want to keep all of the client’s assets with them, but can only provide up to $250,000, the limit the FDIC insures.

Often, the bank or broker will engage with a third-party “deposit broker,” (or sometimes create their own), and resell clients’ deposits to other banks for a higher yield. That brings risks, he said.

“If the originating financial institution were to fail, you can lose access to all of the money sent to those other banks, because you as a depositor don’t have a direct relationship with these banks,” he said. “It’s all through an intermediary.”

Advisors whose clients are concerned about the viability of their banking institution can, if possible given their business channel and restrictions, spread cash deposits around to remain under the $250,000 FDIC insurance limit and diversify institutional exposure.

“As long as the client feels secure about their cash, then they’re likely to feel secure about the rest of their portfolio,” he said.

Tom West, a Virginia-based investment advisor with RIA Real Estate and Investment Advisors, said he’d gotten some phone calls from clients about moving bank deposits above FDIC levels to different banks, even though most are more diversified.

But West said the ongoing banking situation may prompt more prospects to look beyond banks when looking for investment advice and planning, noting that the growth in RIA channels had been outstripping bank brokerage growth for long before the bank crisis. Advisor headcount in the retail bank b/d channel increased by a 0.7% five-year compound annual growth rate, compared with advisor headcount in the RIA channels, which grew by a 3.3% five-year CAGR, according to Cerulli.

“Things were growing significantly before,” he said. “I don’t think SVB is going to slow it down.”

[ad_2]